When I began this newsletter, it was March of 2020. I was updating 18 U.S. companies on factory openings after the initial COVID lockdown. Before I knew it, it turned into hundreds then went viral. I am not a writer. But I do know container shipping and have spent decades working in and out of China for various companies including Shipping Lines and NVOCCs. My point is, now it seems, everyone has a newsletter. But unfortunately, not everyone has the background to analyze the current situation as it pertains to our inbound container supply chain. In the same article, I found one person announcing a crash in rates while their colleague announced a surge in rates. Yeeow, hard to follow? It is no wonder everyone is confused and looking for answers. The good news? Things are not as bad as people would have you believe.

HOT TOPICS FOR JANUARY

BCOs

NVOCCs

OCEAN CARRIERS

PORTS

BLANK SAILINGS

- Maersk and Hapag Lloyd head to the altar.

The Maersk and Hapag Lloyd alliance is creating quite a buzz, and upon hearing about it, I found it to be a logical move. Consider this: MSC has been actively acquiring ships, boasting 79 vessels with a capacity of 5.64 million TEU in the current market. In comparison, Maersk, with 677 vessels, has a capacity of 4.15 million TEU. The significance lies not just in the capacity but in the sheer number of vessels. With 122 more vessels than Maersk, MSC gains the ability to be present in locations where Maersk may not have a representation.

Maersk’s conservative approach is evident with only 36 vessels on order, while MSC has another 118 in the pipeline. The merger of Maersk and Hapag Lloyd makes strategic sense. When all the new vessels are operational, the Gemini Alliance will boast 971 vessels, surpassing MSC’s 917. While this may not be the sole reason for the alliance, it does mean that MSC won’t have a numerical vessel advantage over Maersk. Additionally, Hapag Lloyd stands to gain more opportunities through this collaboration.

The second factor could be related to the affiliation of sister European countries. The dynamics of interaction would be more akin than operating within the framework of The Alliance, which is predominantly Asian driven. Considering the shared mentality of North European countries as opposed to an Asian mindset, this decision makes sense. Both companies are seeking enhanced efficiencies. An example of this difference between cultures was present when Hapag Lloyd announced they were interested in buying Hyundai. Upon this announcement I thought impossible. But I was surprised to see people posting it was a good match. Despite the interest in seeing it happen, I was certain that the Korean Government would never allow foreign ownership of their flagship carrier.

The third factor might be a trial run for a merger. There has been a persistent rumor for quite some time that Hapag Lloyd might be available for acquisition. This alliance could potentially serve as a trial for a Maersk takeover of Hapag Lloyd. The deal allows Maersk to maintain a regularly scheduled service without diverting their focus from their logistics strategy. Habben Jansen articulated it well when he mentioned a “Good Fit.” I believe this possibility has been under consideration for a considerable period. Both companies are cautious in their planning.

2. BCOs

- A Rocky Start to 2024.

- Unprecedented Challenges for 2024.

- Will We See Higher Base Rates for New Contracts?

As we usher in the new year, we find ourselves amidst various challenges, including conflicts in Palestine and Ukraine, a severe drought affecting the Panama Canal, and terrorist attacks on vessels in the Red Sea. Adding to the complexity, the closure of our Southern Border, encompassing key crossings like Laredo and Eagles Pass, has set the stage for a tumultuous start to 2024. Even if these issues are resolved, the repercussions are far-reaching.

It’s prudent to initiate preparations for the upcoming 2024 ocean contract season, and the landscape is posing unprecedented challenges. Geopolitical tensions globally, ongoing ILA negotiations on the east coast, and partial blockages in both the Panama and Suez Canals are reshaping the dynamics of transit and cost considerations, particularly for east coast port users. The previously reliable forecasts and budgets are now subject to increased volatility.

For companies delivering products via east coast facilities, a proactive approach involves sandbagging and padding transit and cost estimates. The alternative of utilizing west coast ports, despite the associated costs of MLB transits, becomes a viable option to mitigate uncertainties in the face of the ever-changing global events. However, with Texas border closures and a significant truck backlog, even this alternative comes with challenges.

Anticipate carriers tightening capacity through blank sailings, creating a container backlog extending into the April-May period. Carriers, facing financial pressures, are compelled to negotiate better contract rates. The severe limitations on vessel transits at the Panama and Suez Canals leave carriers with little choice but to reroute vessels, resulting in extended and alternative routes for east coast-bound vessels.

This situation is likely to impact rates, with carriers considering additional costs for container movement to the east coast. The spread between East Coast and West Coast rates, already exceeding $1,000, reflects the dynamic nature of the shipping industry responding to disruptions. As carriers adjust strategies and pricing models to align with the evolving global trade routes, this spread may further widen. In 2024, a convergence of factors, including geopolitical tensions and canal blockages, sets the stage for potential rate increases, underscoring the need for strategic planning and flexibility in navigating the complexities of the shipping industry. This scenario mirrors the challenges faced in May/June of 2020, indicating a high probability that space and equipment will remain scarce throughout the new contract period, supporting a higher base rate for the 2024/2025 contract year—favoring Ocean Carriers.

Some companies, influenced by higher rates, have delayed new orders temporarily. Although rates have risen, many companies still secure space at their lower contract rates. While the lessons from COVID underscore the importance of risk and change management strategies, the present circumstances, though challenging, do not paint a picture of a major logistics collapse on the immediate horizon. However, it is anticipated that conditions may tighten post Lunar New Year, necessitating vigilance and adaptability in the logistics landscape.

3. NVOCC

- Rate Confusion or Speculation?

- How High Can FAK Spot Rates Go?

- The Ideal Routing to the East Coast.

There have been a lot of media and linked in attention related to the volatility of rates in the transpacific trade. Some say rates are going up while others say rates are going down. I have never heard or read so much noise around what have traditionally been ordinary actions of the carriers. A recent post that copied me asked for my thoughts on relating contracts to the Indexes. (I am not a fan of Indexes since they do not reflect true rates.) Another media blurb had one person noting rates were going up while a person interviewed in the same article noted rates will go down. Yeeow, what confusion. The best way to understand rates and

where they are going is to have an NVOCC as a part of your supply chain. This will allow you to follow the real spot rate scenario.

While everyone has been focused on the up and down of rates, the reality is that for this time of the year, they are quite stable. Carriers have announced a $600 to $1,000 GRI to take effect February 1st. This is highly unlikely. Spot rates took a GRI effective December 15th. And though have fluctuated a little bit seem fairly stable on the FAK spot rates at somewhere around $4,300 to west coast and $5,900 to the east coast. That is not to say there are not better rates available. It is just a matter of your carrier allocation for fixed rates and space availability. Carriers have tried for months in vain to increase the rates. Will this rate increase be any different? It may. Then again, it may not. As I get ready to send this out I am hearing that a February 1st GRI will be implemented bringing the west coast rate to $5,000 and the east coast rate to $7,000. Though it is only a few days away, anything can happen in that time.

Carriers are getting hit with more costs and rerouting vessels to get to Europe and the U.S. East Coast will cost a chunk of change. Low rates are not good for anyone. Yes, BCOs are angry and are trying to clamor for their money back from COVID but if carriers lose money and another carrier gets merged, things will get worse rather than better. Play the long game. NVOCCs are hanging on but margins are slim. Even Flexport announced another round of layoffs. And who will come to the rescue? It seems the canals and the Houthis are teaming up to support higher rates this year. With the Suez all but closed, limitations on the number of vessels passing through the Panama Canal, east coast and gulf containers will have little choice but to move through the west coast. I have heard of at least one NVOCC offering MLB rates to the east and gulf coasts.

If we speculate on the impact on rates, we should take a look at what is happening in Europe. Carriers at one point increased 40’ rates to $5,000/40’ ++. I have heard that MSC reinstituted their Premium Diamond Service. Same service, just more money. Carriers also cut the named account percentage they would handle to 60% in order to push the remaining 40% to the FAK spot rates which they expected to increase. Or so everyone thought. Rates are now back down to $4,100 to $4,300 to N. Europe ports. Demand has been wavering. The better-thanexpected retail sales cleared much of the warehouses of inventory so we may be at the end of our de-stocking period. Many importers, however, decided to take a wait and see attitude to new orders. Let’s see what happens post Chinese New Year. BCOs will need to get ahead of expected delays as vessels get rerouted globally to avoid the Panama and Suez Canals.

By the time you read this, we should be on our 45th or 46th day of the Red Sea crisis. Will operation prosperity resolve the Suez issues? Nearly every carrier now has announced a rerouting schedule. I cannot see any of the shipping lines going back through the Suez Canal in the immediate future. So, what are the options? I have outlined the options in the chart

Note: Many carriers are open to shipping east coast containers on an MLB move via the west coast. Yang Ming it seems is adding a string of vessels to their Vancouver service to move additional containers to the east coast via Vancouver.

above. My recommendation is to stick with the Panama Canal. Though vessel transits through the canal are down, this does not apply to container vessels. Container vessels are still transiting via the canal. Though there is a delay, the real transit time might be not as much as re routing around the Cape of Good Hope.

4. OCEAN CARRIERS

- How Will New Vessel Orders Impact Global Trade?

- Overcapacity May Be Overhyped.

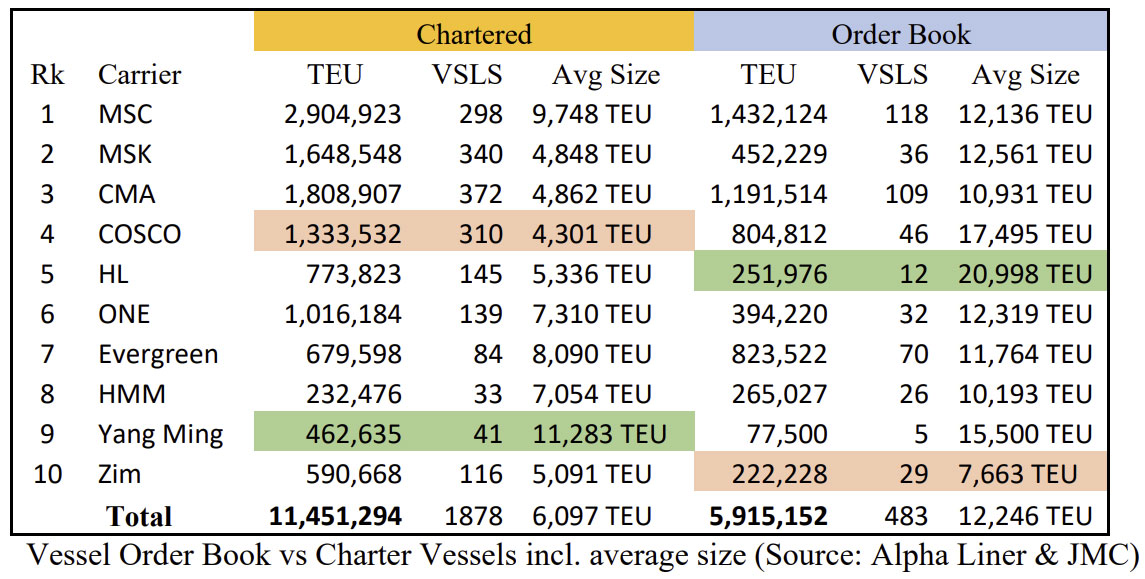

The current global capacity of the top 10 container shipping lines sits at 23,990,456 TEU spread out over 3,595 vessels. The current average vessel size is 6,673 TEU. Yeeow, not as large as one would have imagined. Keep in mind, every one of the top 10 global carriers has a significant presence in Transpacific. In fact, these carriers dominate every major global trade lane. A question that keeps entering my mind is what will the impact on global trade be when the vessels in the new order book are delivered. Below you will note a chart that shows tonnage for vessels on order to include capacity and a comparison with chartered vessels capacity. There are 483 vessels still on order representing 5.9 million TEU of additional capacity. This compares with what is on charter at 1,878 vessels representing 11.45 TEU of capacity. The average sized vessel ordered compared with those chartered will double from 6,097 TEU under charter to 12,246 TEU on order. Recently there has been much speculation about the impact of new vessel capacity on rates for the major global trade lanes, particularly the Transpacific trades. The below chart might illustrate the impact that has fueled much speculation of an impending rate crash.

First let’s dissect the changes we see in the chart below. The red background denotes the carrier with the smallest average size vessel while the green background highlights the carrier with the largest average sized vessel. We see that all carriers are increasing the average sized vessel through their orders for new vessels. The carrier with the smallest vessels on charter is COSCO. So, it may come as no surprise that they have the largest sized vessels on order when it comes to volume and average size; 17,495 TEU average size over 46 vessels. I don’t

Discovering the chart on the next page heightened my enthusiasm as it corroborated my suspicions. The vessel growth trajectory of MSC from February 2021 to May 2023 reveals a noteworthy shift in the ratio of owned vessels to chartered vessels. MSC appears to be reducing its reliance on chartered vessels, opting to deploy vessels from their orders. This trend is marked by a rise in the number of owned vessels and a concurrent decline in chartered vessels. I foresee a similar pattern unfolding across all carriers.

As carriers strategically pivot to increase the proportion of owned vessels relative to chartered ones, the anticipated capacity surge in ocean shipping lines may be more subdued than expected. This shift in strategy could potentially lead to an increase in rates rather than a decrease. The evolving landscape suggests a dynamic scenario in which carrier strategies play a pivotal role in reshaping the dynamics of the shipping industry

- Global Disruption?

- Alternate Options?

- For Now, Cape of Good Hope?

We find ourselves ensnared in what might be aptly described as “the Perfect Storm.” Recent events, such as limitations and blockages in both the Panama and Suez Canals, are compelling shipping lines to reroute through the Cape of Good Hope. Compounding the challenges, the shutdown of our southern border in Texas, including crucial crossings at Laredo and Eagle Pass, lasted for almost a week. What was once a given—open borders and the free flow of global trade—is now facing significant challenges. The landscape of global trade is undergoing a reassessment in the face of these disruptions.

I do not pretend to have the inside scoop on what has been happening on the Red Sea. Many of the posts on the situation show the same map and say the same thing. My recommendation for keeping up with what is going on is to follow Lars Jensen. He provides a daily, and I believe accurate blow by blow update on the tense situation. It seems the “Coalition” has begun fighting back and attacked the Houthi’s missile launchpads, but it is too early to tell what might happen. I do believe that the Houthi’s are fanatics, and they will not be stopped so easily. By the time you read this, we will be in our 46th or 47th day of this conflict. Let’s just hope this ends soon.

So what is our routing? Panama? Suez? Or, Cape of Good Hope? The challenges facing the Panama and Suez Canals have intensified, turning them into significant choke points that are restricting vessel traffic critical for the transportation of containers from Asia to the U.S. East Coast. One canal faces limitations due to extreme weather conditions, while the other is affected by the activities of Houthi Rebels, creating a double whammy for global supply chains. The vessel transit limitations of the Panama Canal due to the extreme drought, has forced carriers to re-route vessels via the Suez Canal. Whoa, hold on there. Where do we go? Panama or Suez? Let’s flip a coin. Actually, the limitations at the Panama Canal are not impacting the container vessels as much as the bulk and tanker ships. My recommendation is book your shipments on vessels transiting the Panama Canal.

In response to the increased demand and better than expected November rainfall, the Panama Canal is adjusting its operations. Due to better-than-expected November rains, the canal will increase the number of daily transits from 22 to 24. Moreover, there might be a deviation from the initially planned reduction to 18 vessels per day on February 1st. The daily transits will be split, with 7 allocated for neo-panamax vessels (8,000 to 13,000 TEU) and 17 for Panamax vessels (under 8,000 TEU). Many carriers, however, have already re-routed vessels to the Suez Canal only to be hit with a hailstorm of attacks on their ships.

Historically, the Suez Canal has been considered an alternative route to the Panama Canal for East Coast-bound containers. However, recent disruptions by missile and drone attacks by Houthi rebels sympathetic to Hamas in their war on Israel, have led to the exploration of a third alternative solution via the Cape of Good Hope. This highlights the need for flexibility in supply chain strategies as companies seek ways to navigate the challenges posed by these vital waterways.

The Suez Canal, a vital waterway for global trade, requires vessels to transit via the Red Sea. However, the entrance to the Red Sea and, subsequently, the Suez Canal entails navigating through the Bab-el-Mandeb Strait. Unfortunately, this strait has become a hot spot for Houthi rebels who have targeted passing vessels. Incidents include the firing upon ships, with at least one container vessel hit by missiles. Furthermore, a car carrier was hijacked and currently remains at a port in Yemen. Yeeow, this is not what I signed up for. But the Bab-el-Mandeb Strait, situated between Yemen on the Arabian Peninsula and Djibouti and Eritrea in the Horn of Africa, serves as the narrowest entrance to the Red Sea, spanning approximately 20 miles (32 kilometers) in width. This strategic location makes it a critical point for vessels transiting to and from the Suez Canal.

Despite these efforts, the dependency on East Coast routings from China and other Asian countries remains challenging, at least in the immediate future. Companies are faced with tough decisions as they explore alternative options, such as rerouting through the Magellan Strait, Cape of Good Hope, or Suez Canal, each with its own set of complexities and longer transits. As I mentioned earlier, my favorite option is to use the Panama Canal. Container vessels are not impacted as much as it sounds. Failing that, many carriers are now offering MLB options via the west coast ports.

6. BLANK SAILINGS

At this point, it is hard to assess the impact of blank sailings since unintentional blank sailings and vessel delays are not necessarily publicized. The rerouting of vessels around the Cape of Good Hope is adding to the blank sailings.

Best Regards,

Jon Monroe

Jon Monroe Consulting